Turning 18 marks the beginning of adulthood, and it’s also the perfect time to take charge of your finances. What should I do when I turn 18 financially? The decisions you make now will have a long-term impact on your financial well-being.

This guide will walk you through the essential financial steps you should take at 18, such as budgeting, saving, investing, and setting long-term financial goals. By implementing these strategies and using tools like a customizable budget template, you’ll be well on your way to financial success. Let’s dive in!

Table of Contents

Key Financial Facts for Young Adults

(Insert Table Here: A table with updated and relevant financial statistics for young adults, showing average savings, spending habits, etc.)

| Fact | Value |

|---|---|

| Average Savings Rate (18-24 years old) | 7% of monthly income |

| Recommended Emergency Fund (18-24) | 3-6 months of living expenses |

| Average Debt for Young Adults | $20,000 (including student loans) |

| Ideal Retirement Savings by 25 | $10,000 – $15,000 |

🔗 Related:

- 👉 How to Build an Emergency Fund

- 👉 How to Budget When You Live Paycheck to Paycheck (And Still Save)

- 👉 How to Pay Off Debt Fast with Low Income

- 👉 What Should I Do When I Turn 18 Financially?

What Should I Do When I Turn 18 Financially?

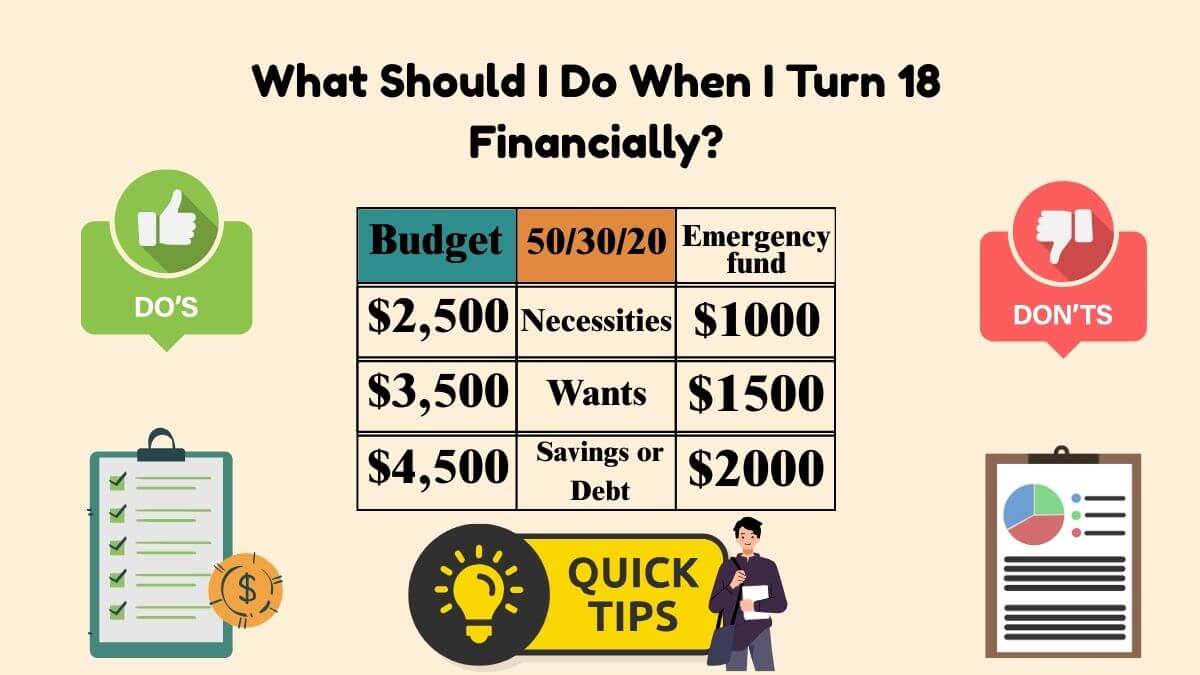

- 1. Start Budgeting

One of the first steps you should take when you turn 18 is to create a budget. Understanding what should I do when I turn 18 financially starts with tracking your income and expenses. Use the 50/30/20 rule — allocate 50% to necessities (like rent and bills), 30% to wants (like entertainment), and 20% to savings or debt. This simple strategy will help you stay on track and work toward your financial goals.

💡 Pro Tip:

Download our free customizable budget template to help you get started. It’s easy to use and fully editable in Google Sheets or Excel.

What Shouldn’t I Do Financially When I Turn 18

While it’s important to take charge of your finances, there are a few financial mistakes to avoid. What should I do when I turn 18 financially? Don’t fall into the trap of overspending on unnecessary items or using credit cards irresponsibly. Always aim to pay off your balance each month and avoid spending money you don’t have. Creating a budget can help you stay focused and prevent these common mistakes.

💡 Pro Tip:

Avoid using credit cards for non-essential items. If you can’t afford something now, don’t charge it to a card. Pay for what you can afford.

Budgeting Skills for Young Adults

As a young adult, mastering budgeting is one of the best financial skills you can develop. Start by categorizing your expenses and tracking your spending regularly. Setting up a budget will allow you to prioritize savings, avoid debt, and reach your financial goals faster.

💡 Pro Tip:

Use apps like Mint or YNAB (You Need a Budget) to track your expenses and ensure you’re sticking to your budget. Download our budget tracker template to customize it according to your needs.

Budgeting Tips for Young Adults

As a young adult, you may face new financial responsibilities, such as paying rent, buying groceries, and covering transportation costs. Budgeting is about balancing your income with these responsibilities, while also saving for your future. The key is to track every penny and make sure you’re saving consistently.

💡 Pro Tip:

Automate your savings. Set up automatic transfers to a savings account each month, so you’re saving first and spending second.

Budget for 20-Year-Olds

When you turn 20, your financial responsibilities may change. Whether you’re getting your first full-time job or paying rent, make sure your budget reflects these changes. It’s also the perfect time to start building an emergency fund, which should cover 3-6 months of living expenses.

💡 Pro Tip:

Start saving for your emergency fund first, then focus on other savings goals like retirement or a down payment on a car or house.

Financial Goals for Your 20s

Setting clear financial goals in your 20s is essential to ensure you’re on the right track. These could include saving for retirement, paying off student loans, or saving for a major purchase, like a car or house. Once you’ve achieved these goals, focus on larger financial objectives.

💡 Pro Tip:

Break down big financial goals into smaller steps. If your goal is to save $10,000 by 25, set a target of saving $500 a month.

Financial Advice for Young Adults

At 18, it’s a great time to start educating yourself about money management. Whether it’s learning about credit scores, how to save for retirement, or how to invest, gaining financial knowledge early will help you make better financial decisions.

💡 Pro Tip:

Read books, listen to podcasts, and follow financial blogs to expand your financial knowledge. Some great books to start with include Rich Dad Poor Dad by Robert Kiyosaki and The Intelligent Investor by Benjamin Graham.

Ways to Make Money for Young Adults

If you want to achieve your financial goals faster, consider ways to earn extra money. Freelancing, side hustles, and online gigs are all excellent opportunities for young adults to supplement their income.

💡 Pro Tip:

Invest in learning new skills. Consider freelancing in areas like writing, graphic design, or digital marketing. These skills can help you earn extra income while gaining valuable experience.

Retirement Planning for Young Adults

Although retirement may seem far off, the earlier you start saving, the better. Opening a Roth IRA or contributing to a 401(k) as soon as you start working will give you a head start. Even small contributions can grow significantly over time thanks to compound interest.

💡 Pro Tip:

Start contributing to retirement accounts now, even if it’s just $50 per month. Every little bit adds up over time.

Best Financial Books for Young Adults

Reading personal finance books can help you build a solid understanding of money management. Books like Rich Dad Poor Dad by Robert Kiyosaki and The Millionaire Next Door by Thomas Stanley offer excellent insights into managing money and building wealth.

💡 Pro Tip:

Invest in your financial education. Start with books that offer foundational financial knowledge, and then move on to more advanced topics like investing and real estate.

Budgeting for Young Adults

Budgeting is the foundation of good financial health. A well-thought-out budget helps you stay on track and ensures that you’re saving for both short-term and long-term goals. Regularly review and adjust your budget as your life circumstances change.

💡 Pro Tip:

Review your budget monthly and adjust for any changes in income or expenses.

Download FREE 2025 Budget Template & Customized Budget Plan?

Start managing your finances today with our customizable budget template. Download it in Excel or Google Sheets and take the first step towards financial independence. Start making smarter financial choices today!

Let me help you build your plan — for free.

Fill out this form to get a personalized monthly budget based on:

- Your income

- Your real expenses

- Your goals (debt-free, travel, fund, etc.)

👉 Tap here to request your custom plan

Why start from scratch? I’ve created a free Excel & Google Sheets budget template tailored for a $2500 monthly income.

📌 Download Your Free Budget Template Here

Frequently Asked Questions (FAQ)

Q1: Why is budgeting important for young adults?

Budgeting helps you control your spending, save for the future, and avoid debt. It’s essential for managing your finances and living within your means.

Q2: What financial mistakes should I avoid at 18?

Avoid using credit irresponsibly, neglecting savings, and living beyond your means. Build good financial habits early for a secure future.

Q3: How much should I save each month?

Aim to save at least 20% of your income. Start with an emergency fund, then move on to other savings goals like retirement and major purchases.

Q4: How can I plan for retirement in my 20s?

Start contributing to retirement accounts like a Roth IRA or 401(k). Even small contributions can grow significantly over time thanks to compound interest.

Q5: What is the 50/30/20 budgeting rule?

The 50/30/20 rule is a simple budgeting method where 50% of your income goes to necessities, 30% to wants, and 20% to savings or debt repayment.